Women face unique challenges when it comes to building their retirement fund. In fact, in "FQ Book 3, High FQ By Design," I devote a whole section on this to discuss 10 money challenges women face. For this article, we will focus on three of them.

1. Gender pay gap – Women are paid less than men for similar jobs held.

2. Career interruptions – Because nature designed women to carry the child in pregnancy and are generally better wired for child-rearing, they are the ones who usually take off from work to do this important job.

3. Longer lifespan – Women live longer than men by an average of five to seven years.

In other words, women have to prepare a larger retirement nest egg from their lower salaries during their shorter work periods! What a challenge!

But you know women, they always manage. And I’d like to help every woman reading this article build that well-deserved strong retirement fund now. Let’s get to it.

1. Maximize your earnings in this male-dominated world.

On average, a woman is paid 82 cents to a dollar. On top of that, studies show that men ask for raises more often than women do. Given this situation, it is imperative for women to negotiate their salaries. Know your worth and don’t settle, ask for that raise and help close that gender pay gap.

Upskill and reskill in order to qualify for higher-paying roles.

Create multiple income streams by doing side hustles that won’t negatively affect your current job.

2. Save and invest as early as possible.

Observing the first basic law of money, saving, is fundamental in your financial journey. If you’re raising girls (and boys too), please make this one of the first lessons you teach them. Then couple that with investing as saving alone is not enough due to inflation.

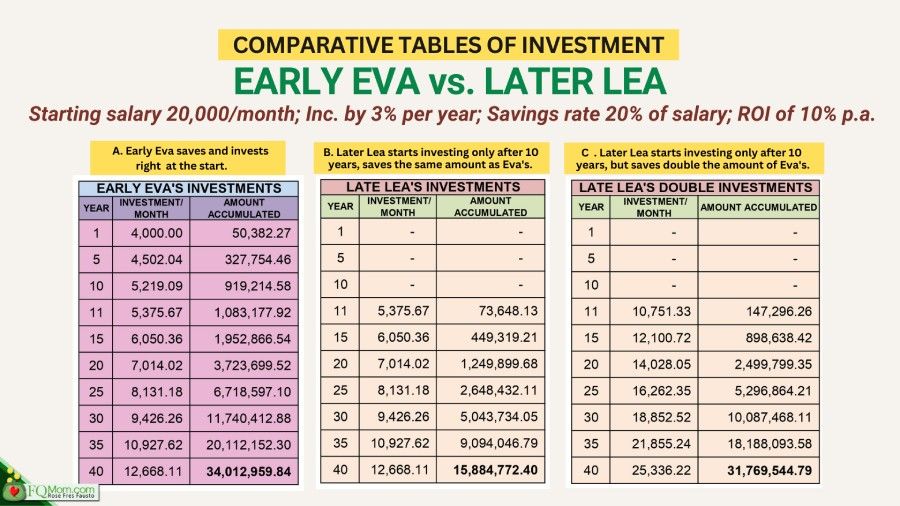

I cannot overemphasize the importance of starting your regular investing ASAP. Let’s just take a look at these two women to drive the point.

Early Eva and Later Lea both started with a salary of P20,000.00 which increased by an average of 3% per year. Early Eva started saving and investing 20% of her salary (P4,000.00) right at the get go, while Later Lea said, “I’ll enjoy my salary first then start saving after 10 years.” Please take a look at the tables below to show you the impact this “later na lang” attitude has on your retirement fund.

The While Early Eva will is able to accumulate P34,012,959.84 upon retirement (see Table 1), the 10 years of delay costs Later Lea more than half of what she could have accumulated. At only P15,884,772.40 (see Table 2), she lost 53% of her retirement fund! In the vernacular, we say, “Nangalahati!” In fact, more than “kalahati” was lost!

What if Later Lea decides to double her investment amounts in order to catch up with Early Eva? What do you think will happen? Will she be able to catch up with Early Eva? Unfortunately, she won’t. Even if Later Lea doubles her investments and does so consistently until retirement, she will only accumulate Php 31,769,544.79, still short by over Php 2 million. Isn’t that mind boggling? That delay of 10 years is so crucial that even if Later Lea invests double the amount for 75% of the time—i.e., 30 out of the 40 years of their investment period, she will still be unable to match Early Eva’s retirement nest egg? That is the power of compounding. That is the reason why we should not delay saving and investing. Time is our biggest ally in investing.

3. Plan for career breaks in advance.

Many women step away from work to care for their children and for some, even those who aren’t their children like aging parents and other relatives. If you intend to do this, plan ahead and consider doing the following—negotiate for flexible work options if possible, maximize any employer benefits available, find ways to earn on a part-time or freelance basis, keep your skills sharp through reading and taking online courses. “Bawal maging mapurol!”

If you are stepping out of your career to care for your children, have that important conversation with your spouse. Make it clear that his earnings are not his alone but belongs to the family. Then continue your regular saving and investing, even if on a reduced amount.

4. Stay financially aware and involved in your marriage.

Even if you are not comfortable with investments, you have to be aware of all the money matters in your family. Do not rely solely on your husband when it comes to finances; otherwise, you will struggle later, and left clueless when any of these happens: separation, widowhood, or financial mismanagement.

I advocate having a family Balance Sheet that is regularly updated so both of you are aware of the goings-on in your finances. Stay involved not only in the budgeting of expenses but also in your investment decisions. Ensure that your name is on key assets such as your house, insurance policies, etc.

Marriage is a partnership and its financial security should never depend entirely on one person.

5. Secure your future health costs.

Since women live longer, expect more healthcare costs in later years. If your employer provides you with HMO or health plan, make good use of it. Before retiring and saying goodbye to your health coverage, study how you can extend the benefit even if you will shoulder the costs once retired. It’s a case-to-case basis so you have to do some pencil pushing to see if the costs are worth the coverage and peace of mind that you will get. Assess this in tandem with what you will continue to get from government health benefits.

Of course, investing in your health is best done by staying active, eating well, having adequate sleep, relaxation and managing stress.

6. Maximize your retirement accounts and benefits.

Think of your retirement fund as a three-legged chair. The three legs are:

a. Government benefits. Keep your SSS or GSIS contributions consistent to qualify for maximum pension.

Use the PERA (Personal Equity and Retirement Account) to avail of its tax advantage and portability.

b. Employer benefits. Many companies offer retirement or provident funds. Contribute the maximum if your employer matches it, do not throw away this free money.

c. Personal investments. Don’t just rely on the above pensions. Build your own retirement portfolio that may have equity, fixed income, real estate, etc. And be an Early Eva in doing this so you maximize the magic of compounding.

7. Automate your saving and investing.

Because you are juggling so many things in life, let the power of inertia or the default bias discussed in "FQ Book 2: Why Financial Education Alone Does Not Work, back-to-back with The Psychology of Money" help you. Make your saving and investing automatic. Talk to the bank that handles your payroll account or check out other platforms that offer this feature of automaticity. This way, you don’t have to think about it every month or so. It also protects you from allowing your emotions to get in the way of your regular saving and investing.

When you do all of these seven items, you will be able to overcome the money challenges you face as a woman and come up with that well-deserved strong retirement fund.

And guess what? Even if we have these money challenges, we actually have inherent strengths that make us great wealth builders. In our next article, we will explore them. Watch out for our next offering titled "The Financial Superpowers Women Have That Make Them Great Wealth Builders."

ANNOUNCEMENTS

1. Want to learn smart money tips from beauty queens? Watch Bianca Guidotti-Santos and Katarina Rodriguez-Barbers share how they deal with money, parenting and values in these two insightful videos:

Click here FQwentuhan with Bianca Guidotti

Click here How a Beauty Queen Manages Money & Family

2. Do you know where you are now in your FQ Journey? Take the FQ Test, click here.

3. Get your copy of the FQ books to start your FQ Journey now. Click here.