Upgrade to High-Speed Internet for only ₱1499/month!

Enjoy up to 100 Mbps fiber broadband, perfect for browsing, streaming, and gaming.

Visit Suniway.ph to learn

Brent crude closed last Friday at $112.57 per barrel – its highest weekly close since 2022 and up by 86 percent year-to-date. The Strait of Hormuz, through which 20 percent of the world’s oil flows, has now been effectively shut for four weeks. Despite an extended ultimatum from President Trump, Iran shows no sign of yielding.

Hormuz remains shut

When the war began on Feb. 28, the IRGC declared the Strait of Hormuz closed and warned that any vessel attempting to pass would be attacked. Within days, strait traffic collapsed by 97 percent. Iran then began selectively allowing ships from friendly nations – China, Russia, India, Iraq and Pakistan – to transit, with some vessels reportedly paying fees in yuan. But the IRGC has since tightened the blockade, closing the strait to any vessel going “to and from” ports of the US, Israel and their allies.

Not even China gets through

But even that fragile arrangement is now in doubt. On March 27, two Chinese container ships operated by Cosco Shipping attempted to exit the Gulf through Hormuz. Despite broadcasting Chinese ownership via their transponders, both were turned back near Iran’s Larak Island. If even Chinese ships cannot pass, no one can count on safe passage.

From disruption to depletion

Saudi Arabia and the UAE have activated bypass pipelines, rerouting crude to the Red Sea and Fujairah. But combined pipeline capacity maxes out at roughly nine million barrels per day – less than half the 20 million that normally transit Hormuz. And the pipelines carry only crude, not refined fuels, LNG, LPG or fertilizer feedstocks. The IEA’s March report called this the largest supply disruption in the history of the global oil market. Gulf producers have cut total production by at least 10 million barrels per day as onshore storage fills up.

Diplomacy stalls

President Trump has twice extended his ultimatum for Iran to reopen the strait, pushing the deadline to April 6. He claims talks are “going very well.” Tehran disagrees. Foreign Minister Araghchi said there have been “no negotiations with the enemy.”

Over the past week alone, Trump said he didn’t want a ceasefire, then said he did. He gave Iran 48 hours to reopen Hormuz, then extended the deadline to five days, then ten. He said he had won the war. Iran denied it all. Markets are confused and have stopped reacting.

Markets slide

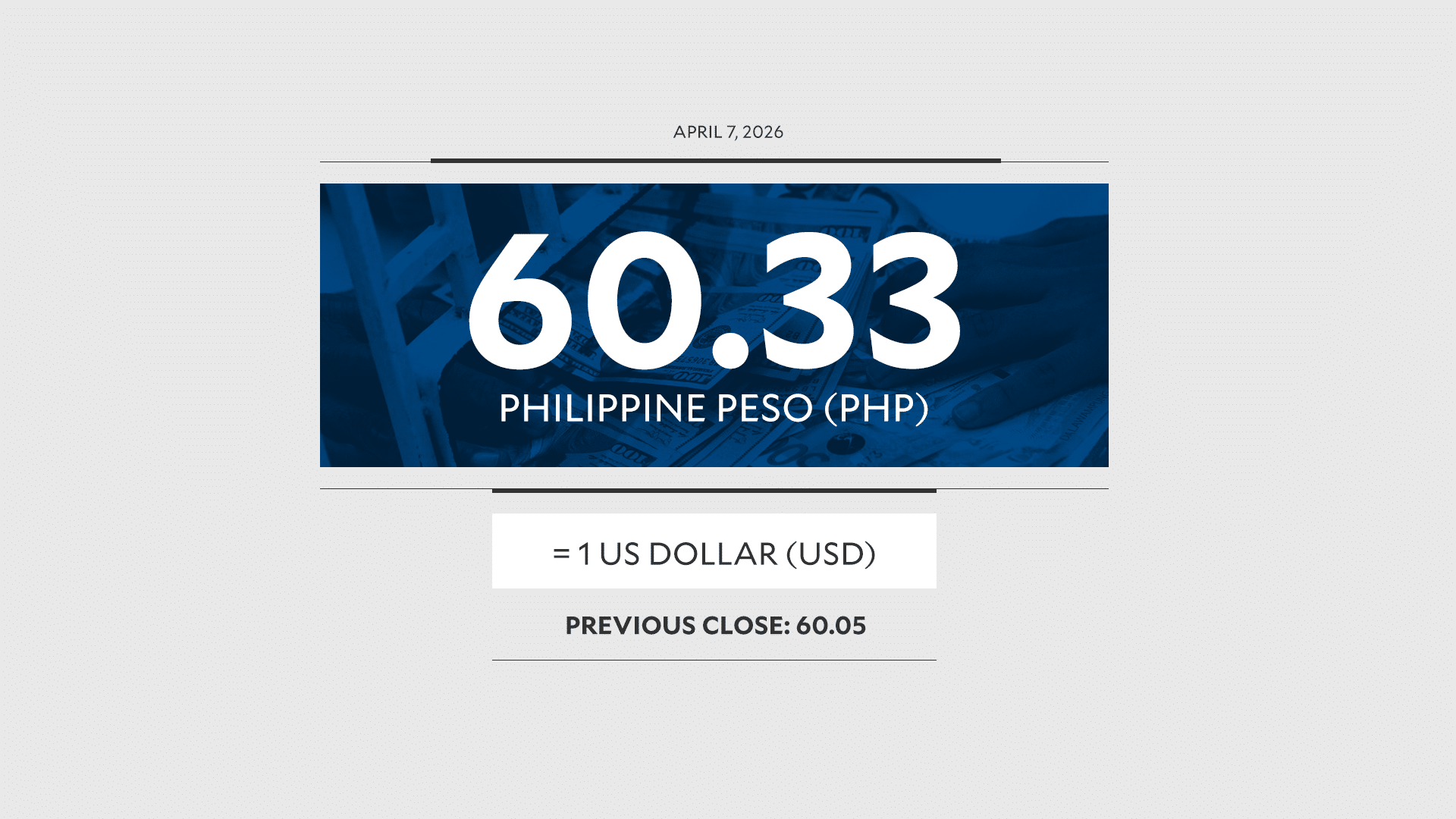

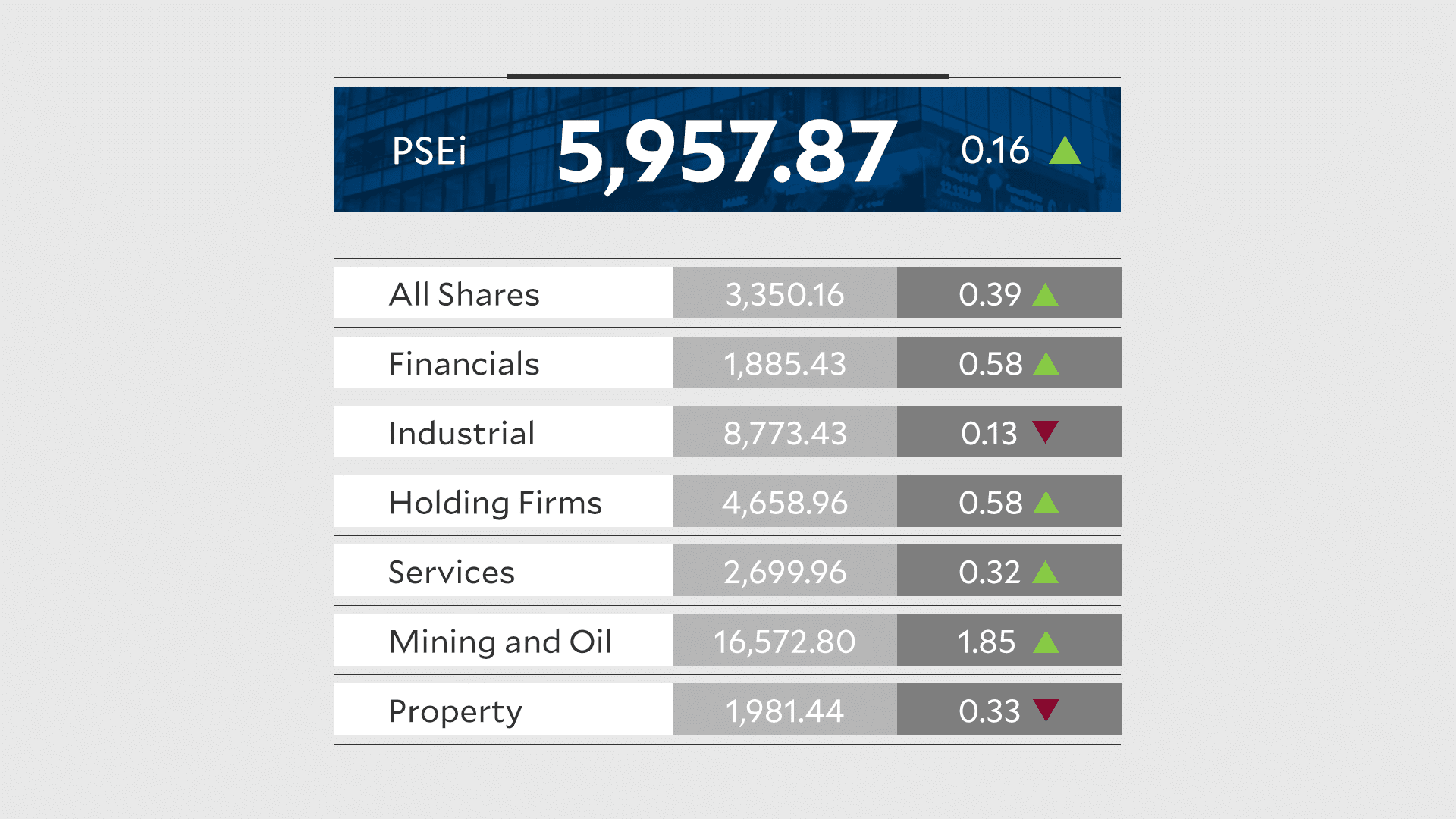

Markets briefly rallied on Monday when Trump first announced talks, but by Friday, with the Cosco ships turned back, Brent surged past $114. The Nasdaq tumbled by 2.2 percent, and the Dow slumped by 1.7 percent, both entering correction territory – defined as a decline of 10 percent or more from a recent peak. The S&P 500 posted its fifth consecutive weekly decline and is teetering on the brink. The PSEi closed at 5,973, down more than nine percent from its pre-war level. The peso hit a new record low of P60.55.

The real battlefield

For all the military dominance, the market is telling a different story. Four weeks of US and Israeli strikes have not broken Iran’s resolve. Falling equities and rising oil have become the barometer by which both sides measure who is winning. Trump watches the Dow and the price at the pump. So does Iran. Every red day on Wall Street validates Tehran’s strategy of keeping the strait shut. The US may have won the military war. The economic war rages on.

Relief measures at home

Fuel prices have roughly doubled since the war began. On March 25, President Marcos signed Republic Act 12316, granting him emergency powers to suspend fuel excise taxes when Dubai crude exceeds $80 per barrel. He also suspended a planned 19 percent transport fare hike, ordered free rides on public transport and launched P5,000 ayuda for over 245,000 transport workers.

Government offices shifted to a four-day workweek. Many private companies have followed with work-from-home arrangements. Starting March 30, over 190 malls, including SM, Robinsons and Ayala, will shorten operating hours to conserve energy.

Scrambling for new supply

The Philippines received its first Russian oil shipment in five years – roughly 700,000 barrels of ESPO blend crude delivered to Petron’s Bataan refinery under a US sanctions waiver. As of March 24, the country’s fuel inventory had dropped to 45 days on average, with diesel at 45 days, LPG at just 23 days, and jet fuel at 38, according to Energy Secretary Garin. The BSP held rates at 4.25 percent last week but raised its 2026 inflation forecast to 5.1 percent – well above the two to four percent target.

Oil will set the direction

Where this war goes, oil goes. And every asset class in the world will follow.

A swift resolution, whether a ceasefire or a partial reopening of Hormuz, would bring down oil prices sharply and trigger a relief rally across equities, currencies and bonds. A protracted standoff, however, would mean higher inflation, tighter monetary policy, slower economic growth, weaker stock markets, and ironically a stronger US dollar.

Philequity Management is the fund manager of the leading mutual funds in the Philippines. Visit www.philequity.net to learn more about Philequity’s managed funds or to view previous articles. For inquiries or to send feedback, please call (02) 8250-8700 or email [email protected].