Upgrade to High-Speed Internet for only ₱1499/month!

Enjoy up to 100 Mbps fiber broadband, perfect for browsing, streaming, and gaming.

Visit Suniway.ph to learn

Keisha Ta-Asan - The Philippine Star

April 20, 2026 | 12:00am

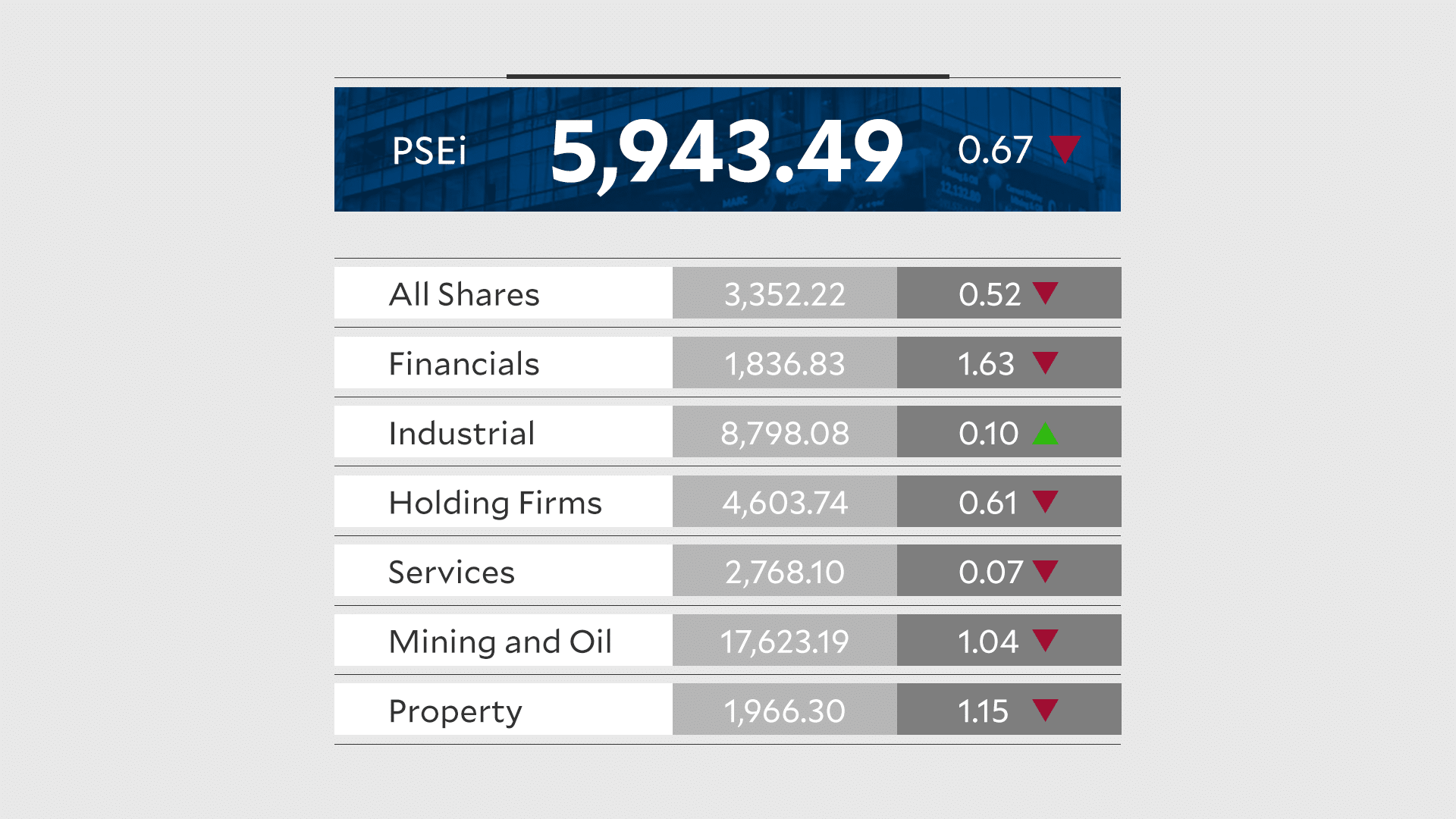

Inflation risks resurface

MANILA, Philippines — Economists are leaning toward a rate hike by the Bangko Sentral ng Pilipinas (BSP) at its Monetary meeting on Thursday as inflation risks resurface following a sharp uptick in March. A majority of analysts expect the BSP to raise policy rates by 25 basis points from the current 4.25 percent, citing mounting second-round effects from the oil shock, peso weakness and broadening price pressures.

However, some economists are calling for a pause, arguing that inflation remains largely supply-driven and demand conditions are soft.

Ruben Carlo Asuncion, chief economist at UnionBank, said a rate increase would help reinforce the central bank’s inflation-fighting stance after March inflation accelerated beyond expectations.

“We expect the BSP to raise the policy rate by 25 basis points (bps) at the Monetary Board’s meeting, especially after March inflation surged to 4.1 percent from 2.4 percent in February – well above the BSP’s earlier projections,” he said.

Asuncion said the sharp rise in inflation highlights the risk of second-round effects and a possible de-anchoring of inflation expectations, especially amid peso-driven imported inflation and persistent pressures from food and transport costs.

“A 25-bp hike would allow the BSP to reaffirm its commitment to price stability, even as it keeps a calibrated and data-dependent stance going forward,” he added.

Similarly, HSBC senior ASEAN economist Aris Dacanay said the BSP is likely to prioritize inflation risks despite a weakening growth backdrop.

“Caught between a rock and a hard place, this week’s meeting will likely be a difficult one for the BSP. The Philippine economy is grappling with an inflation shock that is getting tougher by the day, amid a growth outlook that stumbled well before the conflict in the Middle East escalated,” Dacanay said.

He warned that stagflation risks are increasing and said the BSP may raise its policy rate by 25 bps to 4.50 percent on April 23, potentially marking the start of a tightening cycle, with its duration hinging on how long geopolitical tensions persist.

Dacanay also noted that inflation pressures have intensified after March consumer price growth hit 4.1 percent, breaching the BSP’s two to four percent target band, with second-round effects from higher oil prices already filtering through the economy.

BPI lead economist Jun Neri echoed this view, saying that the balance of risks has shifted toward a more persistent and broad-based inflation environment.

“We expect the BSP to deliver a 25-bp policy rate hike on April 23,” Neri said, adding that full-year inflation could exceed five percent, with monthly prints potentially nearing eight percent if global oil prices remain elevated.

Neri pointed to risks from constrained oil shipments, supply chain disruptions and rising food prices. External vulnerabilities also further complicate the outlook.

“The peso will likely remain under pressure as the situation in the Middle East remains fluid. A sharper depreciation would amplify imported inflation. This forex-inflation feedback loop may ultimately become a binding constraint, and may require tighter policy even in the face of a supply-driven shock,” he said.

Metrobank chief economist Nicholas Antonio Mapa likewise expects a 25-bp hike “to offset budding second round effects caused by oil price shock,” adding that tightening would help “corral inflation expectations that may be fraying due to surging energy costs.”

Jonathan Ravelas, senior adviser at professional services firm Reyes Tacandong & Co., also sees a calibrated move by the BSP.

“A 25-basis-point hike is likely because inflation risks are resurfacing and the BSP doesn’t want to be caught reacting too late,” Ravelas said.

“This is a calibrated preemptive response: small, measured tightening now to anchor inflation expectations, support the peso and preserve credibility, instead of risking much bigger hikes later.”

Still, some economists expect the central bank to keep rates unchanged, citing the supply-driven nature of inflation and weakening domestic demand.

Chinabank chief economist Domini Velasquez said the BSP is likely to “adopt a prudent wait-and-see approach” following its decision to hold rates at 4.25 percent in an off-cycle meeting last month.

“Given the external and supply-driven nature of the inflation shock, we see no immediate need for monetary intervention,” Velasquez said.

She noted that while March inflation reached 4.1 percent, this was “largely due to surging fuel prices and the impact of the rice import ban,” adding that demand-side pressures remain subdued amid slowing household consumption and rising unemployment.

Velasquez also cited government measures to mitigate inflation, including suspended transport fare hikes, fuel subsidies and temporary tax relief on petroleum products.

Meanwhile, Standard Chartered Bank Asia economist Jonathan Koh said the BSP could hold rates for now, noting that the central bank may be reluctant to tighten policy in response to supply-driven inflation where “monetary policy effectiveness is limited.”

He added that inflation expectations remain “well anchored,” while underlying demand-side pressures are still contained.

However, Koh expects the Monetary Board to hike interest rates at its next policy meeting on June 18.